| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.60 Billion |

| Market Size (2030) | USD 5.14 Billion |

| CAGR (2025 - 2030) | 7.40 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East Satellite Communications Market Analysis

The Middle East Satellite Communications Market size is estimated at USD 3.60 billion in 2025, and is expected to reach USD 5.14 billion by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

The Middle East satellite communications landscape is experiencing rapid transformation driven by increasing digital connectivity demands and technological advancement. The region has witnessed substantial growth in mobile connectivity, with smartphone subscriptions projected to expand from 558.69 million in 2022 to 796.66 million by 2028, highlighting the growing need for robust communication infrastructure. This digital evolution is further accelerated by the integration of 5G technology, with regional 5G subscriptions expected to surge from 22.26 million in 2022 to 285.3 million by 2028, creating unprecedented opportunities for satellite communication providers to enhance satellite connectivity solutions and service delivery across various sectors.

The market is witnessing significant investments and strategic initiatives that are reshaping the industry landscape. In October 2023, Saudi Arabia announced a landmark investment of USD 266.57 million to establish its first satellite manufacturing plant, demonstrating the region's commitment to developing indigenous space capabilities. This development is complemented by major contract awards, such as the UAE government's USD 5.1 billion mandate to Yahsat in September 2023 for providing satellite service capacity and managed services over 17 years, highlighting the growing government support for satellite infrastructure development.

Cybersecurity has emerged as a critical focus area within the satellite communications sector, with regional organizations facing increasingly sophisticated threats. The average cost of data breaches in Middle Eastern organizations reached a record high of USD 8.07 million in 2023, representing a 15% increase over the previous three years. This has prompted satellite communication providers to prioritize the implementation of advanced security measures and robust data protection protocols, driving innovations in secure communication technologies and infrastructure resilience.

The maritime and offshore sectors are emerging as key growth drivers for satellite communications, with significant developments in unmanned vessel technologies and port automation. In February 2023, the UAE and Israel collaborated to develop unmanned vessels for maritime threat prevention in the Gulf region, exemplifying the growing intersection of satellite communications with maritime security initiatives. This trend is further supported by regional ports' digital transformation efforts, including the implementation of artificial intelligence and automation technologies at major facilities like DP World and Jebel Ali, creating new opportunities for satellite-based communication solutions in maritime operations and logistics management.

Middle East Satellite Communications Market Trends

The Growth of Internet of Things (IoT) and Autonomous Systems

The Middle East region is experiencing a significant surge in IoT adoption and autonomous systems implementation, driven by the increasing demand for efficient and real-time data connectivity across various industries. The region is projected to reach 1,030 million IoT connections by 2025, highlighting the massive scale of connected device deployment. This exponential growth in IoT devices has created a fundamental need for reliable and widespread connectivity, particularly in remote and challenging environments where traditional communication infrastructure is limited or non-existent. The integration of satellite communications has become crucial in facilitating robust connectivity for IoT devices, enabling businesses to collect, analyze, and utilize real-time satellite data for improved operational efficiency and decision-making.

Recent developments in the region demonstrate the growing emphasis on IoT-satellite integration. In October 2023, MinFarm Tech and Global Beam Telecom announced plans to open a new facility in Business Bay, Dubai, UAE, focused on IoT-over-satellite innovation. This initiative aims to provide customized hardware and connectivity packages specifically tailored to Middle East-based customers requiring precise operational oversight and field-level efficiencies. Additionally, OQ Technology received recognition at the Middle East Technology Excellence Awards in October 2023 for its 5G Narrow-Band IoT and Machine-to-Machine capabilities, which utilize 3GPP standards to offer plug-and-play solutions functioning effectively on both terrestrial and satellite networks. These developments underscore the growing importance of satellite communications in supporting the region's IoT ecosystem and technological advancement initiatives.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Military and Defense Satellite Communication Solutions

The persistent geopolitical tensions and evolving security threats across the Middle East have created a substantial demand for robust and secure satcom solutions in the military and defense sector. The region's total military spending reached USD 184 billion in 2022, marking a 3.2% increase from 2021, with Saudi Arabia leading the expenditure at USD 75 billion and Qatar registering the highest year-over-year spending growth of 27% with USD 15.6 billion. This significant investment in defense capabilities has directly translated into increased demand for sophisticated satellite communication systems that can support tactical operations, strategic defense initiatives, and secure data transmission across military networks.

The defense sector's modernization efforts are evident in recent strategic developments and technological implementations. In March 2023, Israel launched its military intelligence satellite, Ofek 13, demonstrating the region's commitment to enhancing satellite-based surveillance and communication capabilities. Furthermore, in September 2023, Iran's Revolutionary Guards successfully launched the Noor3 imaging satellite into orbit, highlighting the growing emphasis on military satellite applications across the region. These developments are complemented by strategic partnerships and investments, such as the August 2023 collaboration between the Saudi Arabian Military Industries (SAMI) and L3Harris Technologies to establish a new production line for software-defined multi-band radio systems, which aims to strengthen the region's defense communication infrastructure and capabilities.

Segment Analysis: By Type

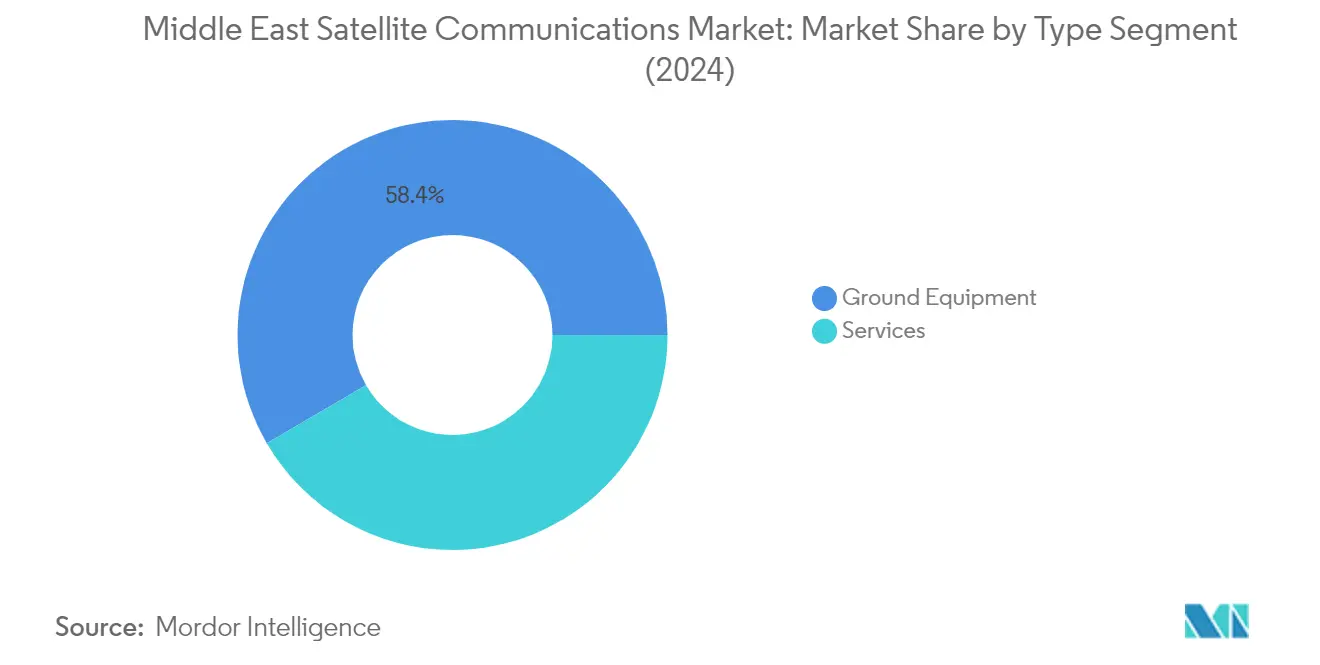

Ground Equipment Segment in Middle East Satellite Communications Market

The Ground Equipment segment dominates the Middle East Satellite Communications market, commanding approximately 58% market share in 2024. This segment encompasses critical infrastructure components, including satellite gateways, Very Small Aperture Terminal (VSAT) equipment, Network Operation Centers (NOC), and Satellite News Gathering (SNG) equipment. The segment's prominence is driven by the increased number of ground stations supporting various activities, such as augmented satellite-based navigation and high-throughput satellite communication services. Furthermore, this segment is experiencing the fastest growth with a projected CAGR of around 10% from 2024-2029, primarily fueled by the rising demand for commercial aviation applications and commercial satellite imagery-based services. The growth is further supported by technological advancements in optics and communication technologies, improving the capabilities of smaller spacecraft for remote sensing and imaging.

Services Segment in Middle East Satellite Communications Market

The Services segment plays a vital role in the Middle East Satellite Communications market, providing essential Mobile Satellite Services (MSS) and Earth Observation Services. This segment focuses on delivering comprehensive satellite services solutions, including two-way voice and data services to moving endpoints such as ships, airplanes, and vehicles. The segment has established itself as a crucial enabler for various applications, including media broadcasting, extension of broadband coverage, setting up of 5G communications systems, and integration of diverse wired and wireless technologies. The services segment particularly excels in providing earth observation capabilities, supporting various sectors, including defense, security, and surveillance applications, while also enabling critical communications in remote and challenging environments across the Middle East region.

Segment Analysis: By Platform

Land Segment in Middle East Satellite Communications Market

The land platform segment dominates the Middle East satellite communications market, holding approximately 40% market share in 2024. This segment encompasses satellite communication solutions specifically designed for terrestrial operations and communication requirements on land, facilitating seamless connectivity, reliable data transmission, and efficient communication services for fixed terrestrial locations, remote sites, and terrestrial infrastructure. The segment's leadership position is driven by the ongoing development of terrestrial infrastructure in the Middle East, including expanding urban areas, industrial zones, and transportation networks, which necessitates robust and reliable communication solutions. Furthermore, this segment is experiencing the fastest growth rate of around 8% during 2024-2029, primarily attributed to the defense and government sector's emphasis on secure and resilient communication services to support national defense and border security. The continuous development of terrestrial infrastructure and increasing emphasis on secure communication services within the defense and government sector are contributing to the sustained growth of the land platform segment in the market.

Remaining Segments in Platform Segmentation

The maritime, airborne, and portable segments collectively represent significant portions of the Middle East satellite communications market, each serving distinct operational requirements. The maritime segment caters to vessels, shipping companies, and offshore industries, providing crucial communication solutions for navigation, tracking, and operational coordination. The airborne segment addresses the specialized communication needs of commercial aircraft, helicopters, and unmanned aerial vehicles, enabling efficient connectivity and data transmission for aerial operations. The portable segment offers flexible and adaptable communication solutions for users requiring on-the-go connectivity and rapid deployment capabilities, particularly valuable in remote locations and temporary work sites. These segments continue to evolve with technological advancements and increasing demand for reliable communication solutions across various industries in the Middle East region.

Segment Analysis: By End-User Vertical

Media and Entertainment Segment in Middle East Satellite Communications Market

The Media and Entertainment segment continues to dominate the Middle East Satellite Communications market, commanding approximately 29% market share in 2024. This segment's prominence is primarily driven by the rising demand for content delivery and the need for seamless, cost-effective distribution solutions across the region. Satellite broadcasting has become increasingly vital for media and entertainment companies in the Middle East, enabling them to distribute content to a broader audience base while developing new business models and entertainment forms. The segment's growth is further supported by the increasing adoption of satellite services by broadcasters and content providers who seek to enhance content delivery with improved capacity and superior end-user experience. The implementation of advanced technologies and infrastructure upgrades by major satellite operators has significantly improved signal strength and bandwidth capabilities, allowing entertainment companies to offer higher content rates accessible to more viewers across the region.

Enterprise Segment in Middle East Satellite Communications Market

The Enterprise segment is emerging as the fastest-growing vertical in the Middle East Satellite Communications market, with an expected growth rate of approximately 8% from 2024 to 2029. This remarkable growth is driven by the increasing digitization among enterprises across the region, coupled with the rising adoption of advanced technologies such as automation, artificial intelligence, and the Internet of Things (IoT). The segment's expansion is further fueled by the benefits associated with satellite communication, including highly secure communication channels, high bandwidth capabilities, low latency, and reliable connectivity at competitive costs. The emergence of Industry 4.0, widespread adoption of cloud-based applications, and the surge in IoT and AI implementation in manufacturing and oil and gas sectors are key trends driving the segment's growth. The demand for sustained high-speed internet connectivity has particularly strengthened the growth of satellite technology for enterprise businesses in the Middle East region, as technology advances have made satellite communication a reliable and cost-effective solution for enterprises requiring constant uptime and high-quality connections.

Remaining Segments in End-User Vertical

The other significant segments in the Middle East Satellite Communications market include Defense and Government, Maritime, and Other End-user Verticals. The Defense and Government sector plays a crucial role in the market, driven by increasing use of satellite communication in intelligence gathering, military operations, surveillance, and disaster management. The Maritime segment continues to be vital for supporting seamless communication and operational efficiency in shipping and offshore operations, particularly given the region's strategic location as a global maritime hub. Other End-user Verticals, including agriculture, forestry, and aviation, contribute to the market's diversity by leveraging satellite communications for specific industry applications such as precision farming, environmental monitoring, and in-flight connectivity services. These segments collectively represent the broad spectrum of satellite communication applications across different industries in the Middle East region.

Middle East Satellite Communications Industry Overview

Top Companies in Middle East Satellite Communications Market

The Middle East satellite communications market features prominent players, including Inmarsat Global Limited, Al Yah Satellite Communications Company, Gulfsat Communications, L3Harris Technologies, E& Etisalat, Eutelsat Communications, Intelsat, Thales Group, Saudi Telecom Company, Raytheon Technologies, and Arabsat. These companies are driving innovation through investments in next-generation satellite technology, software-defined networks, and advanced ground infrastructure development. The industry demonstrates strong operational agility through flexible service delivery models and customized solutions for different end-user segments. Strategic partnerships and collaborations, particularly between regional and global players, are reshaping the competitive dynamics. Companies are expanding their presence through increased ground station networks, enhanced coverage capabilities, and the development of comprehensive satellite service portfolios spanning maritime, defense, enterprise, and media sectors.

Regional Leaders Drive Market Consolidation Trends

The Middle East satellite communications market exhibits a mix of global satellite operators and regional telecommunications conglomerates, with strong government backing playing a crucial role in market dynamics. Regional players like Al Yah Satellite Communications and Arabsat have established themselves as dominant forces through their deep understanding of local requirements and strong government relationships. The market demonstrates moderate consolidation, with established players leveraging their extensive infrastructure and technical expertise to maintain market positions. Strategic partnerships between international satellite operators and local service providers have become increasingly common, enabling comprehensive coverage and enhanced service delivery capabilities.

The market is characterized by significant merger and acquisition activities, particularly focused on expanding technological capabilities and market reach. Companies are actively pursuing vertical integration strategies, acquiring complementary businesses across the value chain from satellite equipment manufacturing to ground segment operations. This consolidation trend is driven by the need to offer end-to-end solutions, achieve economies of scale, and enhance competitive positioning in key market segments such as defense, maritime, and enterprise communications. The industry also witnesses strategic investments in emerging technologies and start-ups, particularly in areas like LEO satellites and advanced ground segment solutions.

Innovation and Integration Drive Future Success

For incumbent players to maintain and expand their market share, focus on technological innovation and service integration has become paramount. Companies must invest in developing advanced satellite infrastructure, including high-throughput satellites and software-defined networking capabilities. The ability to offer integrated solutions that combine multiple frequency bands and orbital configurations will be crucial for meeting evolving customer demands. Successful players are those who can effectively leverage their existing infrastructure while adapting to new technological paradigms and maintaining strong relationships with government stakeholders.

New entrants and challenger companies can gain ground by focusing on niche market segments and developing specialized solutions for specific industry verticals. Success factors include the ability to offer competitive pricing models, innovative service delivery approaches, and superior customer support. The regulatory environment plays a significant role, with companies needing to navigate complex licensing requirements and spectrum allocation policies. End-user concentration in government and defense sectors necessitates strong relationship building and compliance capabilities. While substitution risk from terrestrial networks exists, the unique advantages of satellite network communications in terms of coverage and reliability continue to provide strong market opportunities for well-positioned players.

Middle East Satellite Communications Market Leaders

-

Inmarsat Global Limited (Viasat Inc.)

-

Al Yah Satellite Communications Company PJSC

-

Gulfsat Communications Company

-

L3Harris Technologies Inc.

-

E& ETISALAT and (Emirates Telecommunication Group Company PJSC)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Middle East Satellite Communications Market News

- September 2023 - Es'hailSat, a Qatar-based satellite company, innovated by launching a Playout Service tailored for television broadcasters. This service aims to support the advancement of the media landscape in Qatar and the Middle East, optimizing broadcasters' operations to ensure an uninterrupted and engaging viewer experience.

- February 2023 - A cooperative agreement was signed between DETASAD and Arabsat. Aligned with the Kingdom's Vision 2030 goals, this agreement aims to expand satellite communications services by investing in research and development, offering collaborative advanced technical solutions. These efforts cater to the needs of various sectors across more than 22 countries. The agreement with DETASAD aligns with Arabsat's strategic goals, focusing on providing satellite communications services to both the public and private sectors to meet their connectivity needs, considering the rapidly expanding Saudi and Arabic markets.

Middle East Satellite CommunicationsMarket Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 The Growth of Internet of Things (IoT) and Autonomous Systems

- 5.1.2 Increasing Demand for Military and Defense Satellite Communication Solutions

-

5.2 Market Restraints

- 5.2.1 Cybersecurity Threats to Satellite Communication

- 5.2.2 Interference in Transmission of Data

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Ground Equipment

- 6.1.1.1 Satellite Gateway

- 6.1.1.2 Very Small Aperture Terminal (VSAT) Equipment

- 6.1.1.3 Network Operation Center (NOC)

- 6.1.1.4 Satellite News Gathering (SNG) Equipment

- 6.1.2 Services

- 6.1.2.1 Mobile Satellite Services (MSS)

- 6.1.2.2 Earth Observation Services

-

6.2 By Platform

- 6.2.1 Portable

- 6.2.2 Land

- 6.2.3 Maritime

- 6.2.4 Airborne

-

6.3 By End-User Vertical

- 6.3.1 Maritime

- 6.3.2 Defense and Government

- 6.3.3 Enterprises

- 6.3.4 Media and Entertainment

- 6.3.5 Other End-User Verticals

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Inmarsat Global Limited (Viasat Inc.)

- 7.1.2 Al Yah Satellite Communications Company PJSC

- 7.1.3 Gulfsat Communications Company

- 7.1.4 L3Harris Technologies Inc.

- 7.1.5 E& ETISALAT and (Emirates Telecommunication Group Company PJSC)

- 7.1.6 Eutelsat Communications S.A.

- 7.1.7 Intelsat S.A.

- 7.1.8 Thales Group

- 7.1.9 Saudi Telecom Company (STC)

- 7.1.10 Raytheon Technologies Corporation

- 7.1.11 Arabsat

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Middle East Satellite Communications Industry Segmentation

Satellite communication is the transfer of data and information via satellites orbiting the Earth. It enables long-distance communication by relaying signals between ground stations and satellite receivers in orbit, enabling television broadcasts, internet access, and phone calls.

The Middle East satellite communications market is segmented by type (ground equipment (satellite gateway, very small aperture terminal (VSAT) equipment, network operation center (NOC), and satellite news gathering (SNG) equipment) and services (mobile satellite services (MSS) and earth observation services)), platform (portable, land, maritime, and airborne), and end-user vertical (maritime, defense & government, enterprise, media & entertainment, and other end-user verticals).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | Ground Equipment | Satellite Gateway | |

| Very Small Aperture Terminal (VSAT) Equipment | |||

| Network Operation Center (NOC) | |||

| Satellite News Gathering (SNG) Equipment | |||

| Services | Mobile Satellite Services (MSS) | ||

| Earth Observation Services | |||

| By Platform | Portable | ||

| Land | |||

| Maritime | |||

| Airborne | |||

| By End-User Vertical | Maritime | ||

| Defense and Government | |||

| Enterprises | |||

| Media and Entertainment | |||

| Other End-User Verticals | |||

Need A Different Region or Segment?

Customize Now

Middle East Satellite CommunicationsMarket Research FAQs

How big is the Middle East Satellite Communications Market?

The Middle East Satellite Communications Market size is expected to reach USD 3.60 billion in 2025 and grow at a CAGR of 7.40% to reach USD 5.14 billion by 2030.

What is the current Middle East Satellite Communications Market size?

In 2025, the Middle East Satellite Communications Market size is expected to reach USD 3.60 billion.

Who are the key players in Middle East Satellite Communications Market?

Inmarsat Global Limited (Viasat Inc.), Al Yah Satellite Communications Company PJSC, Gulfsat Communications Company, L3Harris Technologies Inc. and E& ETISALAT and (Emirates Telecommunication Group Company PJSC) are the major companies operating in the Middle East Satellite Communications Market.

What years does this Middle East Satellite Communications Market cover, and what was the market size in 2024?

In 2024, the Middle East Satellite Communications Market size was estimated at USD 3.33 billion. The report covers the Middle East Satellite Communications Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle East Satellite Communications Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Middle East Satellite Communications Market Research

Mordor Intelligence delivers a comprehensive analysis of the satellite communications industry. We leverage extensive expertise in SATCOM and VSAT technologies. Our research thoroughly examines the satellite telecommunication infrastructure, including ground station facilities, earth station operations, and satellite terminal deployments across the Middle East. The report provides detailed insights into satellite technology developments, satellite data management, and emerging trends in satellite internet, satellite phone services, and satellite broadband solutions.

Stakeholders gain valuable understanding of space communications dynamics through our detailed analysis of satellite network architectures and satellite communication system implementations. The report, available as an easy-to-download PDF, covers satellite service offerings, satellite broadcasting capabilities, and innovations in satellite communication device technology. Our research encompasses satellite transmission protocols, satellite connectivity solutions, and space telecommunication advancements. It also examines satellite equipment deployment and satellite infrastructure development throughout the region.